L.L. Speer letter to George H. Moore - April 28, 1917

Transcript

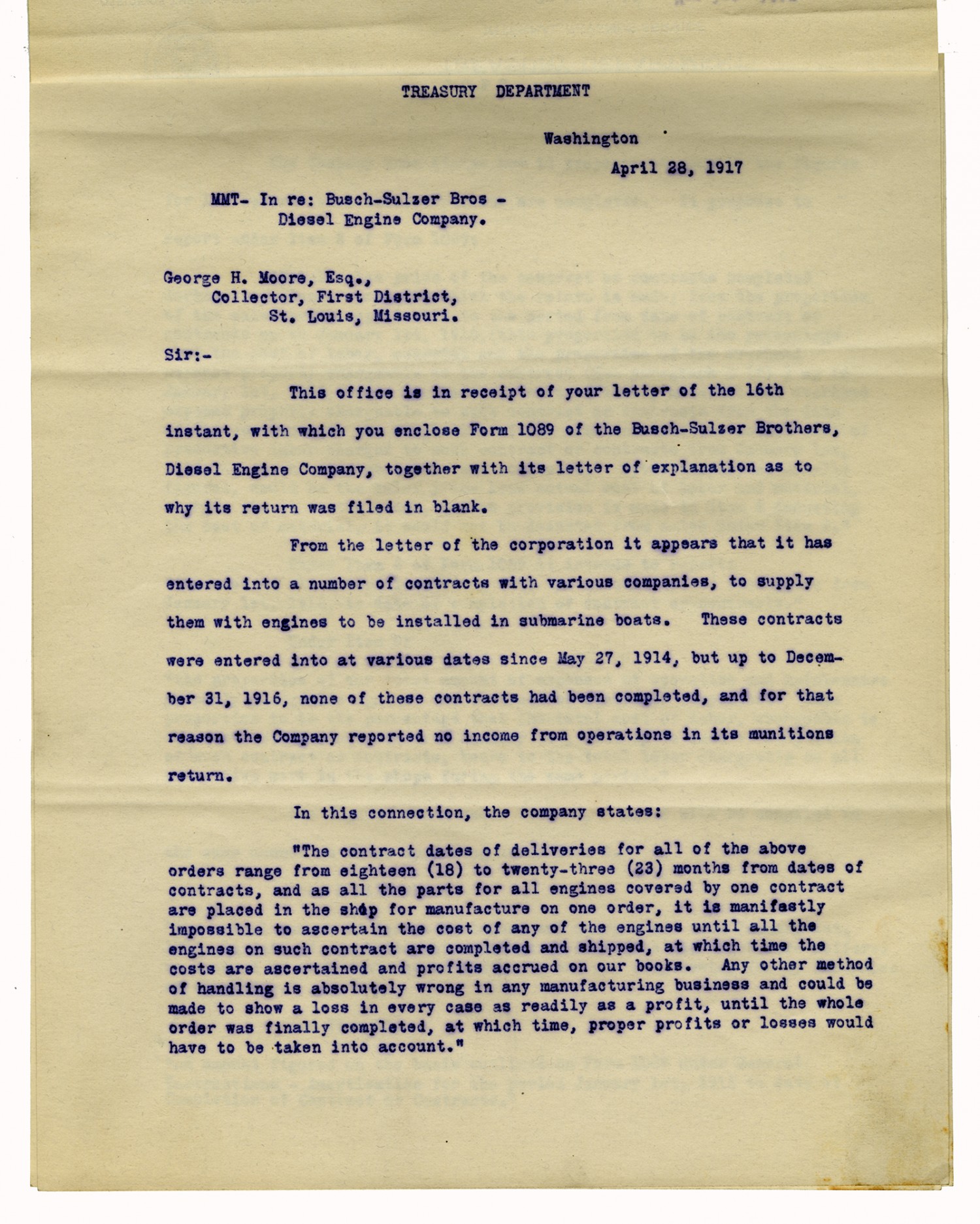

TREASURY DEPARTMENT Washington April 28, 1917 MMT- In re: Busch-Sulzer Bros - Diesel Engine Company. George H. Moore, Esq., Collector, First District, St. Louis, Missouri. Sir:- This office is in receipt of your letter of the 16th instant, with which you enclose Form 1089 of the Busch-Sulzer Brothers, Diesel Engine Company, together with its letter of explanation as to why its return was filed in blank. From the letter of the corporation it appears that it has entered into a number of contracts with various companies, to supply them with engines to be installed in submarine boats. These contracts were entered into at various dates since May 17, 1914, but up to December 31, 1916, none of these contracts had been completed, and for that reason the Company reported no income from operations in its munitions return. In this connection, the company states: "The contract dates of deliveries for all of the above orders range from eighteen (18) to twenty-three (23) months from dates of contracts, and as all the parts for all engines covered by one contract are placed in the shop for manufacture on one order, it is manifestly impossible to ascertain the cost of any of the engines until all the engines on such contract are completed and shipped, at which time the costs are ascertained and profits accrued on our books. Any other method of handling is absolutely wrong in any manufacturing business and could be made to show a loss in every case as readily as a profit, until the whole order was finally completed, at which time, proper profits or losses would have to be taken into account."

Transcript

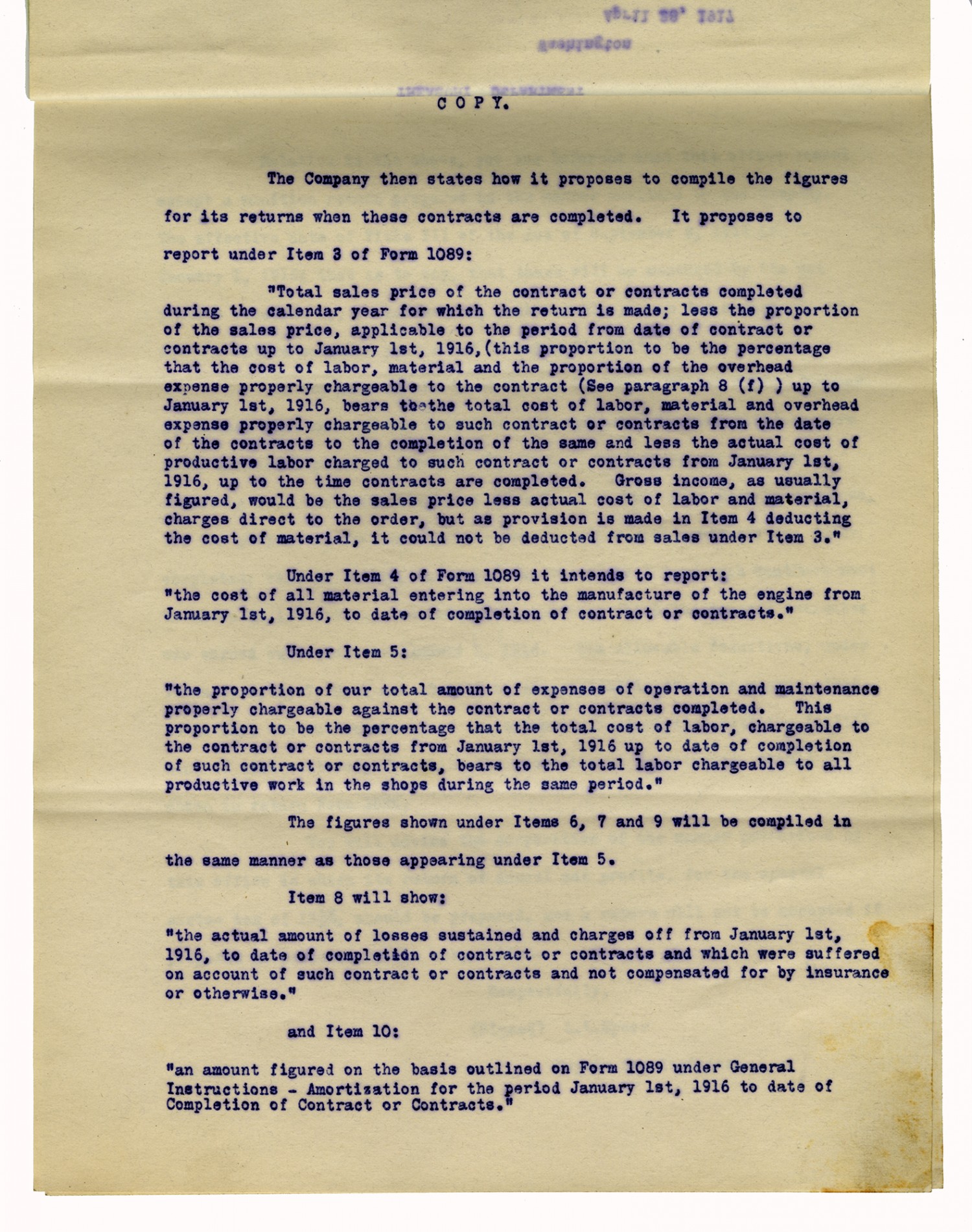

COPY The Company then states how it proposes to compile the figures for its returns when these contracts are completed. It proposes to report under Item 3 of Form 1089: "Total sales price of the contract or contracts completed during the calendar year for which the return is made; less the proportion of the sales price, applicable to the period from date of contract or contracts up to January 1st, 1916, (this proportion to be the percentage that the cost of labor, material and the proportions of the overhead expense properly chargeable to the contract (See paragraph 8 (f)) up to January 1st, 1916, bears thethe total cost of labor, material and overhead expense properly chargeable to such contract or contracts from the date of the contracts to the completion of the same and less the actual cost of productive labor charged to such contract or contracts from January 1st, 1916, up to the time contracts are completed. Gross income, as usually figured, would be the sales price less actual cost of labor and material, charges direct to the order, but as provision is made in Item 4 deducting the cost of material, it could not be deducted from sales under Item 3." Under Item 4 of Form 1089 it intends to repot: "the cost of all material entering into the manufacture of the engine from January 1st, 1916, to date of completion of contract or contracts." Under Item 5: "the proportion of our total amount of expenses of operation and maintenance properly chargeable against the contract or contracts completed This proportion to be the percentage that the total cost of labor, chargeable to the contract or contracts from January 1st, 1916 up to date of completion of such contract or contracts, bears to the total labor chargeable to all productive work in the shops during the same period." The figures shown under Items 6, 7 and 9 will be compiled in the same manner as those appearing under Item 5. Item 8 will show: "the actual amount of losses sustained and charges off from January 1st, 1916, to date of completion of contract or contracts and which were suffered on account of such contract or contracts and not compensated for by insurance or otherwise." and Item 10: "an amount figured on the basis outlined on Form 1089 under General Instructions - Amortization for the period January 1st, 1916 to date of Completion of Contract or Contracts."

Transcript

Relative to the above, you are informed that this office cannot accept a munition return prepared in the manner outlined by the Company. The effective date of Title III of the Act of September 8, 1916 is January 1, 1916; that is to say, that taxes will be measured by the net profits received by, or accrued to, each taxable person for a part of, or for the entire calendar year ended December 31, 1916. In the case of the Busch-Sulzer Brothers, Diesel Engine Company it appears that none of its contracts with various submarine builders were fully performed prior to December 31,1916. Therefore, any profits resulting from contracts completed subsequent to that date must be returned, for the purpose of the tax, for the year in which such contracts are fully competed; that is to say, the gross amount received from each contract must be shown in its return, and not that proportion which the company estimates was earned subsequent to January 1, 1916. Its allowable deductions, under Items 4,5,6,7,8,9 and 10 will be ascertained in the same manner, that is to say, the entire amount of the expenses in connection with the fulfillment of each contract, for which the gross income is returned, should be show in return Form 1089. You will advise the corporation of the manner prescribed by this office in which its return of annual net profits, for the special excise tax of 12 1/2%, should be prepared, and a return will not be accepted if prepared as proposed by the corporation. Respectfully, (Signed) L.L. Speer Deputy Commissioner GVN-BKH

Details

| Title | L.L. Speer letter to George H. Moore - April 28, 1917 |

| Creator | Speer, L.L. |

| Source | Speer, L.L. Letter to George H. Moore. 28 April 1917. Busch-Sulzer Collection. Wisconsin Historical Society, Madison, Wisconsin. |

| Description | Letter from L.L. Speer, the Deputy Commissioner of the Internal Revenue Service, to George H. Moore, collector for the Internal Revenue Service. This letter concerned the Munitions Manufacturer's Tax, which implemented a 12,5% tax on companies who produced munitions for the federal government. Speer explained that the Busch-Sulzer brothers Diesel Engine Company was in fact responsible for paying this tax. |

| Subject LCSH | Diesel engine; Submarine boats; Busch-Sulzer brothers Diesel engine company |

| Subject Local | WWI; World War I; Munitions Manufacturer's Tax |

| Contributing Institution | Wisconsin Historical Society |

| Copy Request | Transmission or reproduction of items on these pages beyond that allowed by fair use requires the written permission of the Wisconsin Historical Society: 608-264-6535 |

| Rights | The text and images contained in this collection are intended for research and educational use only. Duplication of any of these images for commercial use without express written consent is expressly prohibited. |

| Date Original | April 28, 1917 |

| Language | English |