George H. Moore letter to Busch-Sulzer Brothers - December 28, 1916

Transcript

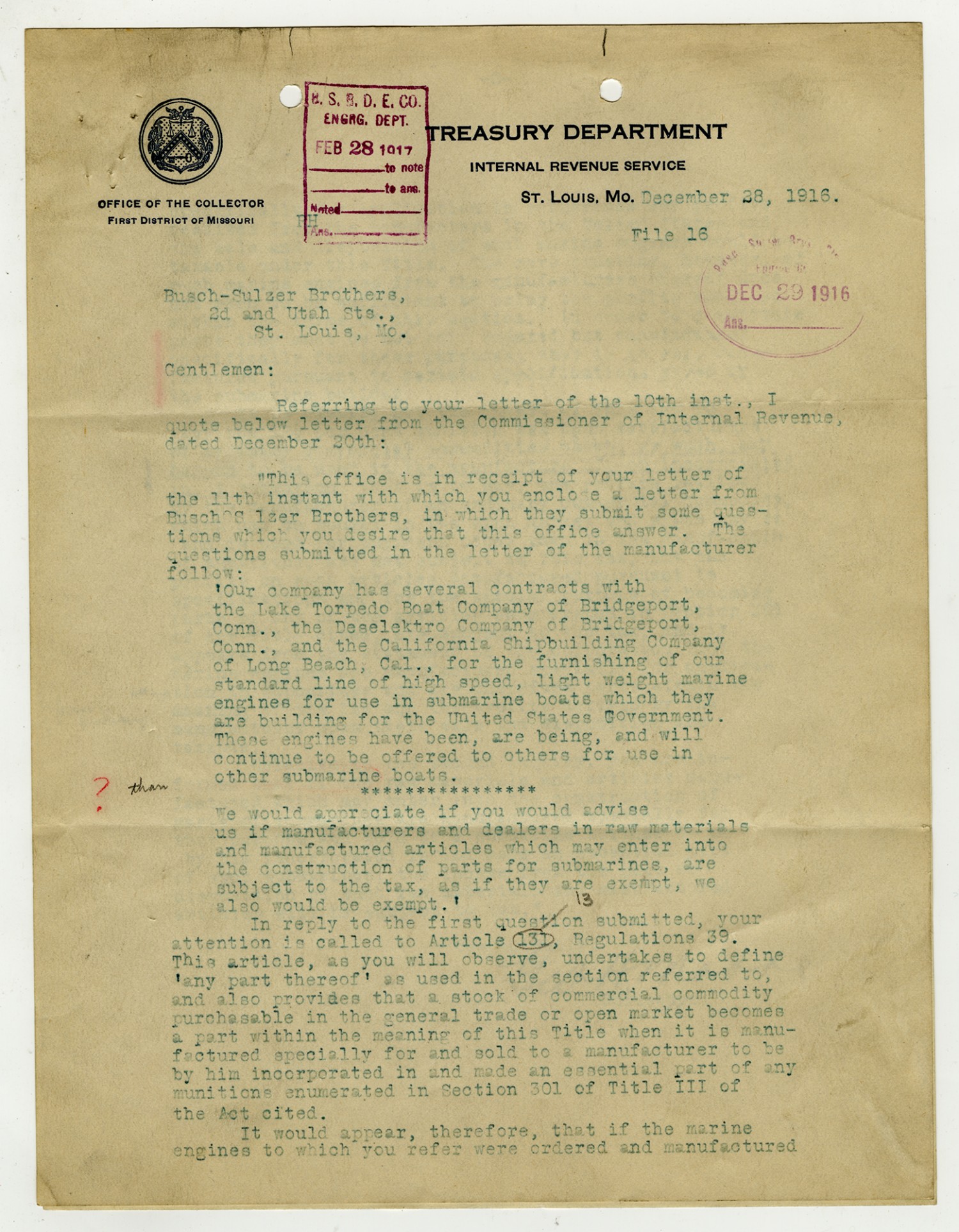

[Treasury Department letterhead] [stamp] B.S.B.D.E.CO. ENGNG. DEPT. [February] 28 1917 to note to ans. Noted Ans. December 28, 1916. File 16 [stamp] Busch-Sulzer Bros. Diesel Engine Co [December] 29 1916 Busch-Sulzer Brothers, 2d and Utah Sts., St. Louis, [Missouri] Gentlemen: Referring to your letter of the 10th inst., I quote below letter from the Commissioner of Internal Revenue, dated December 20th: "This office is in receipt of your letter of the 11th instant with which you enclose a letter from Busch Sulzer Brothers, in which they submit some questions which you desire that this office answer. The questions submitted in the letter of the manufacturer follow: 'Our company has several contracts with the Lake Torpedo Boat Company of Bridgeport, [Connecticut], the Deselektro Company of Bridgeport, [Connecticut], and the California Shipbuilding Company of Long Beach, [California], for the furnishing of our standard line of high speed light weight, marine engines for use in submarine boats which they are building for the United States Government. These engines have been, are being, and will continue to be offered to others for use in other submarine boats. We would appreciate if you would advise us if manufacturers and dealers in raw materials and manufactured articles which may enter into the construction of parts for submarines, are subject to the tax, as if they are exempt, we also would be exempt. In reply to the first question submitted, your attentions is called to Article 131, Regulation 39. This article, as you will observe, undertakes to define 'any part thereof' as used in the section referred to, and also provides that a stock of commercial commodity purchasable in the general trade or open market becomes a part within the meaning of this Title when it is manufactured specially for and sold to a manufacturer to be by him incorporated in and made an essential part of an munitions enumerated in Section 301 and Title III of the Act cited. It would appear, therefore, that if the marine engines to which you refer were ordered and manufactured

Transcript

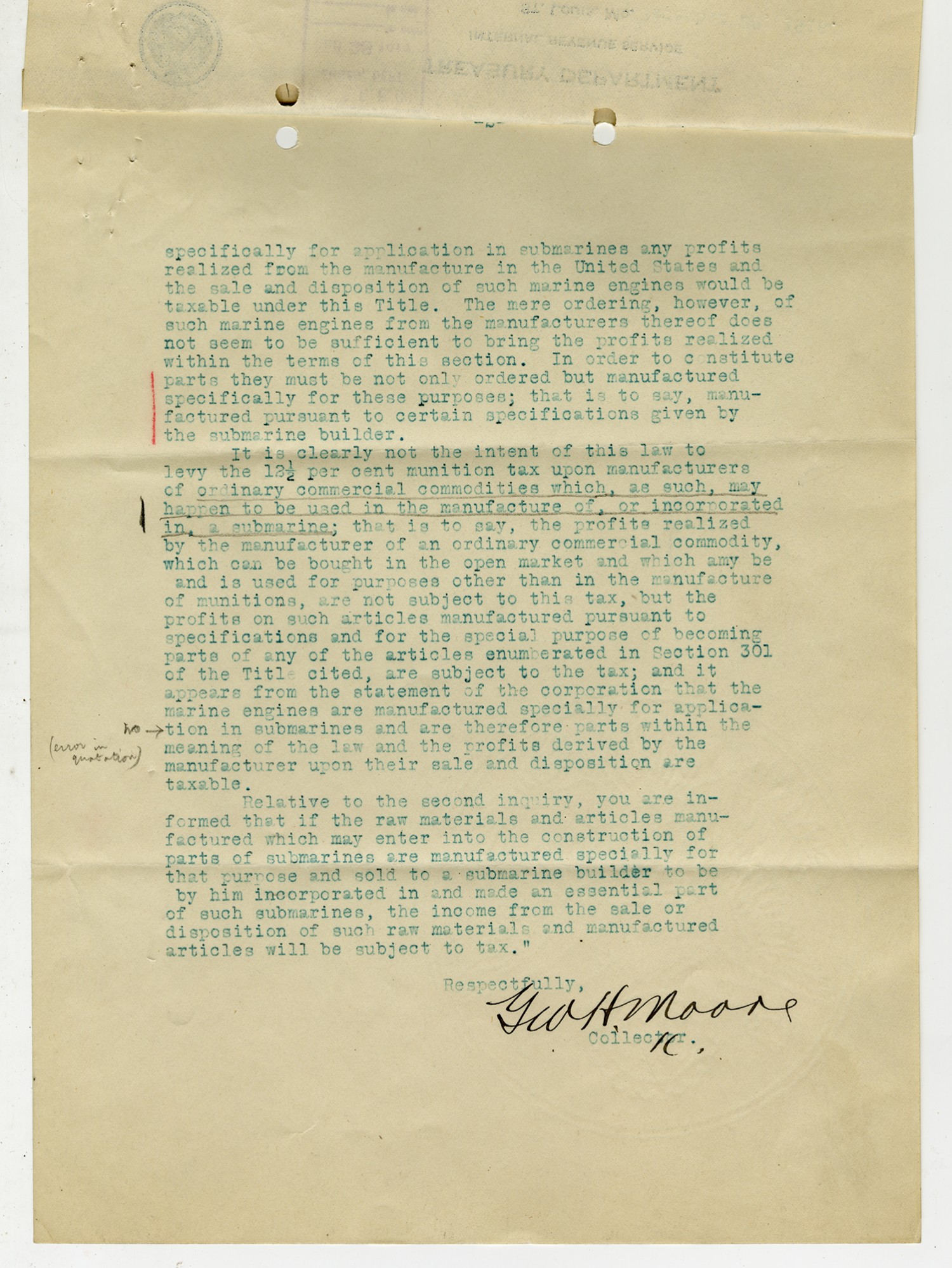

specifically for application in submarines any profits realized from the manufacture in the United States and the sale and disposition of such marine engines would be taxable under this Title. The mere ordering, however, of such marine engines from the manufacturers thereof does not seem to be sufficient to bring the profits realized within the terms of this section. In order to constitute parts they must be not only ordered but manufactured specifically for these purposes; that is to say, manu-factured pursuant to certain specifications given by the submarine builder. It is clearly not the intent of this law to levy the 12 1/2 per cent munition tax upon manufacturers of ordinary commercial commodities which, as such, may happen to be used in the manufacture of, or incorporated in, a submarine; that is to say ; the profits realized by the manufacturer of an ordinary commercial commodity, which can be bought in the open market and which amy be and is used for purposes other than in the manufacture of munitions, are not subject to this tax, but the profits on such articles manufactured pursuant to specifications and for the special purpose of becoming parts of any of the articles enumerated in Section 301 of the Title cited, are subject to the tax; and it appears from the statement of the corporation that he marine engines are manufactured specially for application in submarines and are therefore parts within the meaning of the law and the profits derived by the manufacturer upon their sale and disposition are taxable. Relative to the second inquiry, you are informed that if the raw materials and articles manufactured which may enter into the construction of parts of submarines are manufactured specially for that purpose and sold to a submarine builder to be by him incorporated in and made and essential part of such submarines, the income from the sale or disposition of such raw materials and manufactured articles will be subject to tax." Respectfully, Geo H Moore Collector.

Details

| Title | George H. Moore letter to Busch-Sulzer Brothers - December 28, 1916 |

| Creator | Moore, George H. |

| Source | Moore, George H. Letter to Busch-Sulzer Brothers. 28 December 1916. Busch-Sulzer Collection. Wisconsin Historical Society, Madison, Wisconsin. |

| Description | Letter from the collector for the Internal Revenue Service of St. Louis, George H. Moore, addressed to the gentlemen of the Busch-Sulzer company. Moore addressed the company's inquiry concerning the application of the Munitions Manufacturer's Tax on their product. He explained that under this law, the company will be taxed for the marine engines they produce specifically for the U.S. Government. |

| Subject LCSH | Diesel engine; Submarine boats; Busch-Sulzer brothers Diesel engine company |

| Subject Local | WWI; World War I; Munition Manufacturer's Tax |

| Contributing Institution | Wisconsin Historical Society |

| Copy Request | Transmission or reproduction of items on these pages beyond that allowed by fair use requires the written permission of the Wisconsin Historical Society: 608-264-6535 |

| Rights | The text and images contained in this collection are intended for research and educational use only. Duplication of any of these images for commercial use without express written consent is expressly prohibited. |

| Date Original | December 28, 1916 |

| Language | English |